Buying your first home can feel exciting and overwhelming at the same time, especially when you are looking at new construction in a community like Springfield Village. You want low-maintenance living, a smart monthly payment, and fewer surprises after closing. This guide walks you through what to know about Springfield Village townhomes or twinhomes, from pricing and HOA costs to inspections, contracts, and first-time buyer financing. Let’s dive in.

Springfield Village at a glance

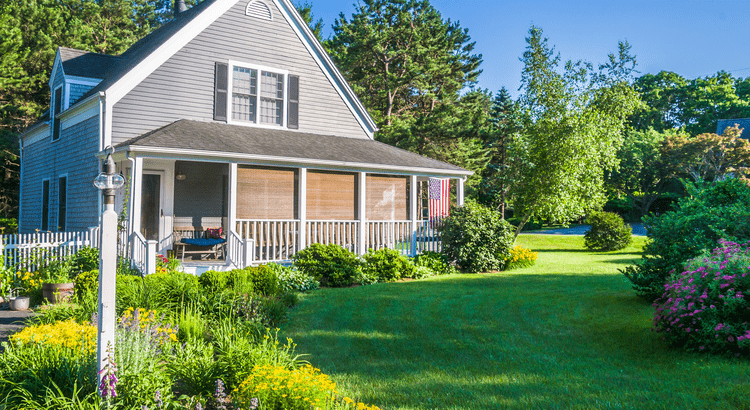

Springfield Village is being marketed as a new low-maintenance attached-home community in the Clemmons and Winston-Salem area. According to Arden Homes, pricing starts in the low $400s, and the community is located on Springfield Farm Road behind West Forsyth High School.

Public records and marketing materials describe the attached homes as both townhomes and twinhomes. That matters because you may see both terms while researching listings, contracts, or HOA details. It is best to mirror the community’s own language rather than assume one label applies everywhere.

There is also a difference in public sources about the total number of homes. Arden and the Village of Clemmons site plan describe the new attached-home section as 26 units on about 13.01 acres, while the HOA site describes Springfield Village as having 127 homes. If you are considering a purchase here, that is a good question to clarify early so you understand exactly which section of the neighborhood you are buying into.

What first-time buyers may like here

For many first-time buyers, Springfield Village offers a mix of newer construction and lower exterior upkeep. Arden’s brochure highlights nearby conveniences such as Publix, Novant Health of Clemmons, Tanglewood Park, Jerry Long YMCA, and access to Clemmons and downtown Winston-Salem.

The builder brochure also shows two main floor plans, the Addison and the Finley, at about 1,711+ and 1,726+ square feet. Some options include added second-floor space and screened or covered porch layouts. If you want a home that feels more spacious than an apartment or smaller starter home, these plans may be worth a closer look.

Budget beyond the mortgage

One of the biggest first-time buyer mistakes is focusing only on the principal and interest payment. Your true monthly housing cost may also include property taxes, homeowners insurance, mortgage insurance if your down payment is under 20%, and HOA dues.

The Consumer Financial Protection Bureau explains that HOA dues are usually paid directly to the HOA and are not typically part of your monthly mortgage servicer payment. Fannie Mae guidance also recognizes that monthly housing expense can include mortgage, taxes, insurance, and HOA fees. In other words, you need to budget for the full picture.

The CFPB also says closing costs often run about 2% to 5% of the purchase price. That means your upfront cash needs may include:

- Down payment

- Due diligence fee or builder deposit, depending on the contract

- Earnest money

- Lender fees

- Prepaid taxes and insurance

- HOA-related costs

- Attorney and closing charges

If you are buying in the low $400s, those numbers can add up quickly. A realistic budget before you start touring homes can help you shop with confidence.

First-time buyer assistance in North Carolina

If you are buying your first home in Springfield Village, you may qualify for state-level help. The North Carolina Housing Finance Agency says the NC Home Advantage Mortgage offers fixed-rate financing with up to 3% down payment assistance, and the NC 1st Home Advantage Down Payment may provide $15,000 to eligible first-time buyers and veterans.

Townhouses are listed as eligible property types. Current eligibility details on NCHFA’s site include a 640 or higher credit score, owner occupancy within 60 days, and income limits up to $152,000.

That does not mean every buyer or every loan scenario will qualify. It does mean that if down payment or cash to close is your biggest hurdle, it is smart to explore these options early before you commit to a builder contract.

Understand HOA costs and rules

Before you buy any attached home, take time to understand the HOA. This is one of the biggest quality-of-life and budgeting factors for first-time buyers.

Springfield Village’s HOA site says membership is required for all homeowners. It also says annual dues are $175, there is a $50 title-transfer administrative fee, and the community has a rental restriction.

According to the HOA information, dues support:

- Entrance and common-area maintenance

- Lighting

- Bookkeeping and mailing costs

- Reserve funding

- A common park area with benches, picnic areas, swings, and playground equipment

Arden’s community marketing also states that the HOA covers exterior lawn care and landscaping, roof repair and replacement, brick and siding repair and replacement, and common-area maintenance. That sounds appealing, but it should lead to an important follow-up question: what is still your responsibility as the owner?

Ask for clear answers about:

- Interior repairs

- Insurance responsibilities and deductibles

- Limited common areas

- Windows, doors, and exterior trim responsibility

- Driveways, patios, porches, and fencing, if applicable

- Rules that affect pets, parking, or leasing

In North Carolina, HOAs are governed by laws such as the Planned Community Act and Condominium Act, but the NC Legislative Library notes that HOAs are not regulated by a state or federal agency in the way many buyers assume. That makes reviewing the governing documents even more important.

Property taxes matter too

Taxes may have a bigger effect on your monthly payment than you expect. Forsyth County lists its FY 2025-26 tax rate at 53.52 cents per $100 of value, and the Village of Clemmons lists a residential tax rate of 15 cents per $100.

There is an important detail here. The Village of Clemmons notes that a Clemmons mailing address does not automatically mean a property is inside village limits. If you are comparing payments, make sure your lender and attorney are using the correct tax assumptions for the specific property you plan to buy.

Forsyth County also notes that property taxes are ordinarily prorated at closing. That means you may owe or receive tax adjustments as part of your final settlement figures.

Builder contracts need close review

New construction contracts are not something you want to skim. In North Carolina, the NC Real Estate Commission explains that an offer must be in writing and signed by all parties to become enforceable, and it notes that a separate new-construction Offer to Purchase and Contract was developed for these types of transactions.

The same source explains that the due-diligence fee is generally paid to the seller when the contract is accepted, and it is usually nonrefundable if you terminate, except in certain seller-breach situations. If a builder also requires a deposit, you should ask exactly how that deposit is handled and whether separate refund rules apply.

The CFPB’s homebuying guidance also makes two points first-time buyers should remember:

- You do not have to use the builder’s affiliated lender.

- You should ask for contingencies tied to financing and a satisfactory inspection.

Those details can protect your money and give you more room to make a careful decision.

Why inspections still matter on new homes

A brand-new home is still a home under construction, and mistakes can happen. That is why an independent inspection matters, even if the property has never been lived in.

The CFPB recommends that buyers schedule a home inspection as soon as possible and attend if they can. It also reminds buyers that an inspection is different from an appraisal.

For a Springfield Village attached home, your inspection checklist should pay close attention to:

- Roof lines and drainage

- Windows and doors

- Exterior finish and shared-wall details

- Grading around the home

- HVAC performance

- Plumbing and electrical systems

- Garage and driveway finish

- Areas that may later overlap with HOA maintenance responsibility

The approved site plan shows public water and sewer plus individual driveway permits, which can also help frame your questions about utilities and site design. If you are buying a resale home in the neighborhood or an inventory home that has sat vacant for a long time, Forsyth County notes in its first-time homebuyer assistance policy that homes unoccupied for more than 12 months can be treated as existing homes for assistance purposes and may need added inspections such as radon or pest checks.

Closing day details to prepare for

As closing gets closer, details matter. The CFPB says you must receive your Closing Disclosure three business days before closing, which gives you time to verify your loan costs, taxes, insurance, and HOA-related charges.

If you are using Forsyth County assistance, the county says newly constructed homes must have a Certificate of Occupancy before closing, and closings in this area are handled by a licensed attorney in the Winston-Salem and Forsyth County jurisdiction. Even if you are not using county assistance, those are helpful benchmarks to keep in mind as your timeline moves forward.

Smart questions to ask before you buy

If Springfield Village is on your shortlist, bring these questions with you:

- Is this home part of the 26-unit attached section, and what documents confirm that?

- What are the current HOA dues and transfer fees?

- What exactly does the HOA maintain, and what stays with the owner?

- Are there rental or leasing restrictions?

- What floor plan is this, and what options or upgrades are included?

- What builder deposits, due-diligence fees, and earnest money are required?

- When, if ever, are deposits refundable?

- Can you use your own lender and inspector?

- What property tax assumptions are being used for the estimated payment?

- Has the home received its Certificate of Occupancy?

These questions can help you compare homes more clearly and avoid surprises after you go under contract.

How to buy with more confidence

Your first home purchase does not have to feel like guesswork. When you understand how Springfield Village is structured, what the HOA covers, how North Carolina new-construction contracts work, and what your full monthly cost may be, you can make a more informed decision.

If you want help comparing floor plans, reviewing costs, or asking the right questions before you sign, reach out to Jerri Banner. You deserve clear guidance and steady support as you take this next step.

FAQs

What is Springfield Village in Forsyth County?

- Springfield Village is marketed as a low-maintenance attached-home community near Clemmons and Winston-Salem, with public materials describing the new attached section as 26 townhomes or twinhomes on Springfield Farm Road.

What do first-time buyers need to budget for in Springfield Village?

- In addition to the mortgage, you should plan for taxes, insurance, possible mortgage insurance, HOA dues, closing costs, and any due-diligence fee, earnest money, or builder deposit required by the contract.

What HOA fees and rules apply in Springfield Village?

- Public HOA information says owners must join the HOA, annual dues are $175, a $50 title-transfer fee applies, and there is a rental restriction, but you should confirm current rules and responsibilities before closing.

What floor plans are offered in Springfield Village?

- Arden’s brochure shows two main plans, Addison and Finley, at about 1,711+ and 1,726+ square feet, with some options for added second-floor space and porch features.

What first-time buyer assistance may work for Springfield Village townhomes?

- The North Carolina Housing Finance Agency says eligible buyers may use programs such as the NC Home Advantage Mortgage and NC 1st Home Advantage Down Payment, and townhouses are listed as eligible property types.

What inspections should buyers consider for a Springfield Village attached home?

- Buyers should still get an independent inspection and pay close attention to roofing, drainage, windows, doors, HVAC, plumbing, electrical, exterior finishes, and any items that may overlap with HOA maintenance.

What should buyers know about new-construction contracts in North Carolina?

- Buyers should understand that offers must be signed to be enforceable, due-diligence fees are often nonrefundable, and builder deposits may have separate rules, so contract terms should be reviewed carefully before acceptance.